Margin, Margin Loans, and my Aha! Moment

I recently got our fiscal house in order.

I recently paid off all of our credit cards and other loans except, of course, for things like the mortgage, student loans.

But that’s fine since those loans are either covered – see also rental – or on maintainable student loan payment plans that are, luckily, within budget.

The thing that blew me away was this:

Margin Loans

In all my days of persuing getting our fiscal house in order I used: debt-consolidation, personal loans for things like travel or otherwise, I was – and this is embarrasing to say – even sometimes trading assets to cover debt related to consumption!

Very, very silly on my part. (If the National Association of Ecomomists or whatever group I took the exam for my bachelors wants to take my “card” away so be it)

I could have been taking out loans against my own assets instead.

HELOCs, Credit Cards, Personal Loans.

HELOC

The most interesting thing that comes to mind would be – for those with a home with some equity – HELOCs: Home Equity Lines of Credit.

Backed by the value and equity of your home you take out a line of credit with some terms and an interest rate and you can use the money or not but it’s there. It’s a nice lifeline to have.

Interest rates are usually in line with mortgage rates. Options exist to pay just the interest. And there’s usually a timeframe in which 7-10 years it works like a credit card with a very good interest rate and then it migrates into a more “normal” loan with a payoff term.

CREDIT CARDS

Most everyone understands how these work. You get inundadated with them in the mail. I think credit card companies have been taken in as apprentices by the Sith Lords that are drug dealers.

A lot of these offers come with incentives like 0% interest on new purchases, 0% interest for X number of months on balance transfers, or go the other way; tons of incentives by way of points, airline miles, etc., etc.

The downside is the insane interest rates. 20-31+%. The reason being it’s not backed by any assets. The HELOC is. Mortgages are. Auto loans are. Credit cards are legit instant credit loans everytime you want to buy Chipotle on your fancy credit card.

(You might not think your situation is dire until you realize you’re taking a loan out to buy lunch…)

It gets even more interesting if you can use the credit card companies against them by transferring loans from one card to a new one with a 12 or 18 month 0 interest. BUT buyer beware! They often charge a one time fee 1-5% or so on the balance being transferred. So that 0% introductory rate is really a 5% loan to pay down your existing loan. And boy howdy if you don’t pay it off it converts to a normal credit card balance. That’s the gamble. Make sure you know what you’re doing.

So, if you’re a credit card company how do you sleep at night? Is it not enough to know that you’ll get the income from the interest when the loan starts accruing the interest when the balance isn’t paid off and the full rate kicks in, you have to charge a balance transfer fee? Seriously?

PERSONAL LOANS

Like vultures to a corpse bankers and their non-banking entities (front ends with good websites and apps that source loans and then sell them to other banks) are foaming at the mouth to get you into loans.

There’s usually a flow. You’ve seen it if you’ve ever done anything at Bankrate.com or similar places.

You fill out a set of questions and that form turns into a payload that goes to a set of banks that then all offer you something.

I recall selecting “consolidate loans” as my answer to why I am seeking debt with such self loathing. (As with any trade there’s always someone on the other side so it stands to reason my self loathing was met with glee)

Anyway …

Finally Margin Loans

I realize all of this is a long winded, pretentious way of saying “if you have assets just take loans out against them you dumb dumb…”

Robinhood

I moved over from ETrade to Robinhood when ETrade enforced a 2-factor login where I couldn’t use a passkey or even a 2-factor TOTP app of my choice i.e Google Authenticator, my 1Password vault etc. While that was very, very annoying the most compelling case to join Robinhood was two-fold:

- A very, very good user interface.

- IRA match. For 5-bucks a month (cost of the Gold program) it’s 3%, for non-members it’s 1%.

That’s a lot of scratch. Free money. And the math works out even with the subscription.

So it was a no-brainer.

Anyways, I haven’t looked back. Use the link to sign up it’s a referral link but it’s a really nice service.

I opened an individual account and threw all but the emergency fund into a reasonable portfolio.

The theory is: the market will return, on average, 7-9+% per annum and that’s a lot compared to bonds, savings accounts, CDs, money market funds, etc etc.

Money Market Funds for example would be perferrable probably since there’s very little risk. And my ALLY bank account for example is paying ~3.5% in interest on savings accounts with 0 risk, yeah, I still am bullish on the market so here we are. Heck, if not MM funds just short duration T-Bills.

Here’s the crux:

I can leave my ETFs and things in the market growing, earning dividends, doing what they do while taking out a loan against them when needed with no credit check, disbursement in a few days, with no term to pay it back UNLESS the value of the equities and other assets the loan is based on falls and just accrues interest at a very low rate.

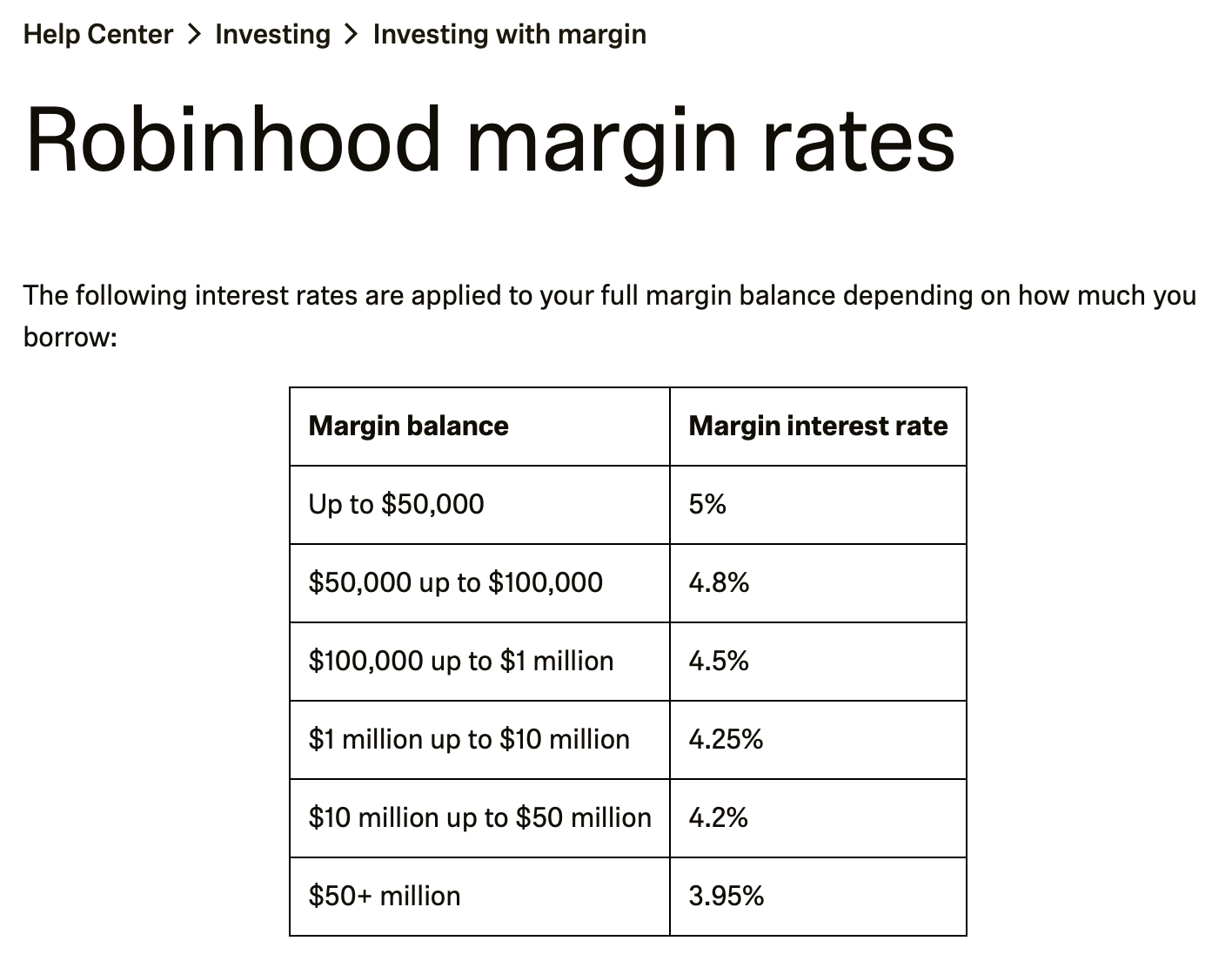

ref: https://robinhood.com/us/en/support/articles/margin-rates/

ref: https://robinhood.com/us/en/support/articles/margin-rates/

Look what’s wrong with this picture. I can take a loan against my equities for 5% and – a Robinhood perk, the first 1k is loaned at 0%! – which means 2k could be loaned out at an effective 2.5% rate!

Here maybe this will help:

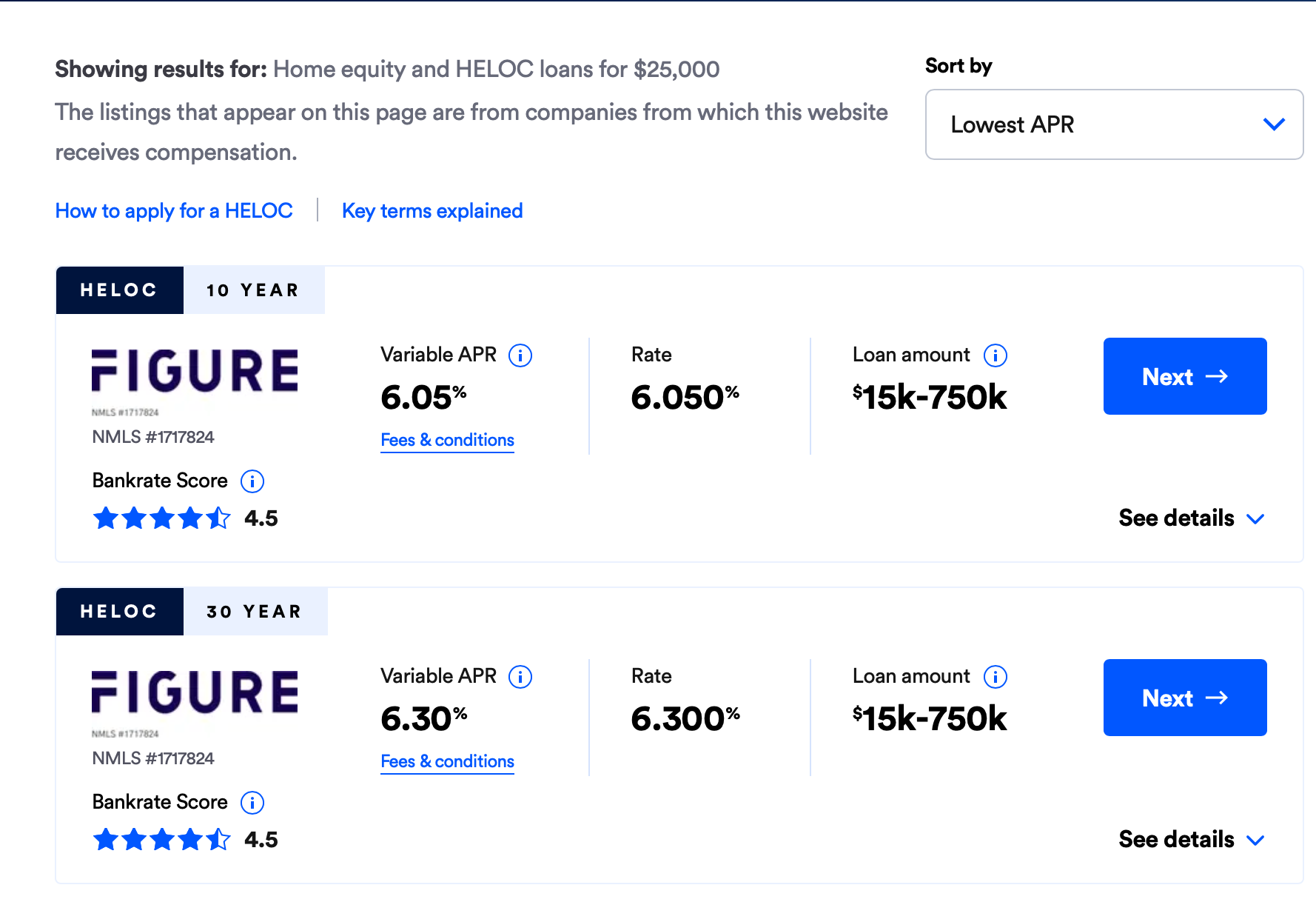

ref: https://www.bankrate.com/home-equity/heloc-rates/?zipCode=97070

ref: https://www.bankrate.com/home-equity/heloc-rates/?zipCode=97070

A VARIABLE! (the margin loan is a fixed rate!) rate loan against your home! where a “margin call” equivalent would mean losing your home… vs just some contracts that give someone legal ownership of some percentage of a companies cashflows aka a stock certificate.

INSERT MIND BLOWN EMOJI here.

That’s basically it.

So …

So if you have a 5-10-15-20k+ in cash that is in a doing nothing savings account throw it into a robust, simple, safe but growing portfolio and be able to take loans out against it.

I think this beats the standard, super-duper safe savings account even though the account grows with compounding interest (each month that interest is paid it’s paid on the balance so future month’s are paying interest on ever larger balances, it snowballs) because one can take loans out against the assets while they’re still “in the market” earning you dividends, growing, etc! You can’t do that with a savings account.

Conclusion

This is how the really wealthy stay wealthy. I am not there, nor will I ever be. I just think it’s cool to have access to something similar. And to be clear, I’ve not had a chance to now. I am not going to go long stocks and things with leverage. I do not want to lose my shirt, house, or sanity.

You’re some Keto-addicted rocket man from South Africa and have no real income. But for some insane, bonkers reason, shares in your electric car company keep outpacing all sane valuations and so your wealth keeps increasing. Oh and btw you’re being awarded more shares based on performance.

So the tax-free way to live the billionare lifestyle is this:

2026 Jan take out 1M against your 100B in equities.

2026 Feb your equities are now worth 100.1B.

2026 Mar you “pay back” your 1M from Jan with increases made since then. Oh and you get more shares, options, RSUs, whatever.

Rinse and repeat.